How to Budget Your Money in Canada (Real Example)

“Parween, how do I budget my money?”

If you’ve been wondering how to budget your money, especially in your 20s, this real client example will show you exactly how to do it.

In response to receiving this question hundreds of times from money coaching clients over the years, let’s walk through a real budgeting plan I created for my client Diya.

Diya is a 28-year-old living in Ontario, earning $78,000 per year working in the public health sector.

She lives at home with her parents, which I always have to asterisk as a normal cultural occurrence in many South Asian households, where adult children of immigrants commonly live at home until they are married.

Her monthly fixed expenses looked like this:

- $300 rent (to her parents)

- $55 cell phone

- $80 gym membership

- $44 subscriptions

- $725 car expenses (payment, gas, insurance)

Her goals were clear:

- pay off credit card debt

- build savings

- start working toward long-term goals like a down payment and investing

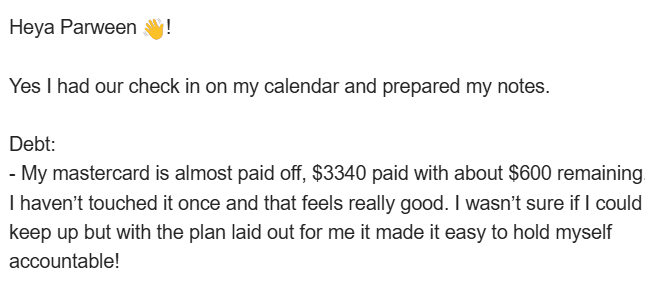

She carried a recurring balance of approximately $3,900 on her Mastercard and had $0 in savings.

And emotionally?

Diya felt ashamed that she had been working for 4 years and had nothing to show for it in her bank account.

Where Is Your Money Going? (Step 1 of Budgeting)

The question becomes: where is the rest of Diya’s income going?

Before creating a budgeting plan, we started with a 3-month financial audit of her credit and bank statements.

This is the first step I recommend to anyone trying to figure out how to budget money.

Diya was adamant that she “wasn’t spending lavishly.”

But the reality of her transactions painted a different picture.

She was overspending by -$440/month, even though her fixed expenses only made up 27% of her income.

That means she was spending:

👉 the remaining 73% of her income

👉 and more

…which is what created her ongoing debt cycle.

This is why, before creating a budget, it’s critical to understand where your money is actually going.

Without this step, most budgets fail, not because you lack discipline, but because the plan isn’t grounded in reality.

Why Budgeting Feels Hard (Scarcity + Money Trauma)

One of the biggest reasons budgeting doesn’t work is not math. It is behaviour.

Diya grew up with hard-working immigrant parents.

There was always enough money for necessities, but never extra for:

- new clothes

- school trips

- going out with friends

She even experienced bullying for not having the “cool” things growing up.

So when she started earning her own income?

She began revenge spending, buying herself the things she was deprived of as a child.

This is more common than you think, especially for daughters of immigrants navigating money for the first time.

At the time, saving and budgeting didn’t feel safe for Diya.

There was internal resistance because budgeting felt like restriction, and restriction reminded her of childhood.

But here’s what I told her:

Spending every dollar to heal your inner child will keep you stuck in the same cycle of scarcity you’re trying to escape.

Because despite earning a good income, she was still:

- stressed about unexpected expenses

- overwhelmed thinking about buying a home

- unsure how she would ever build wealth

The Budgeting Plan That Actually Worked

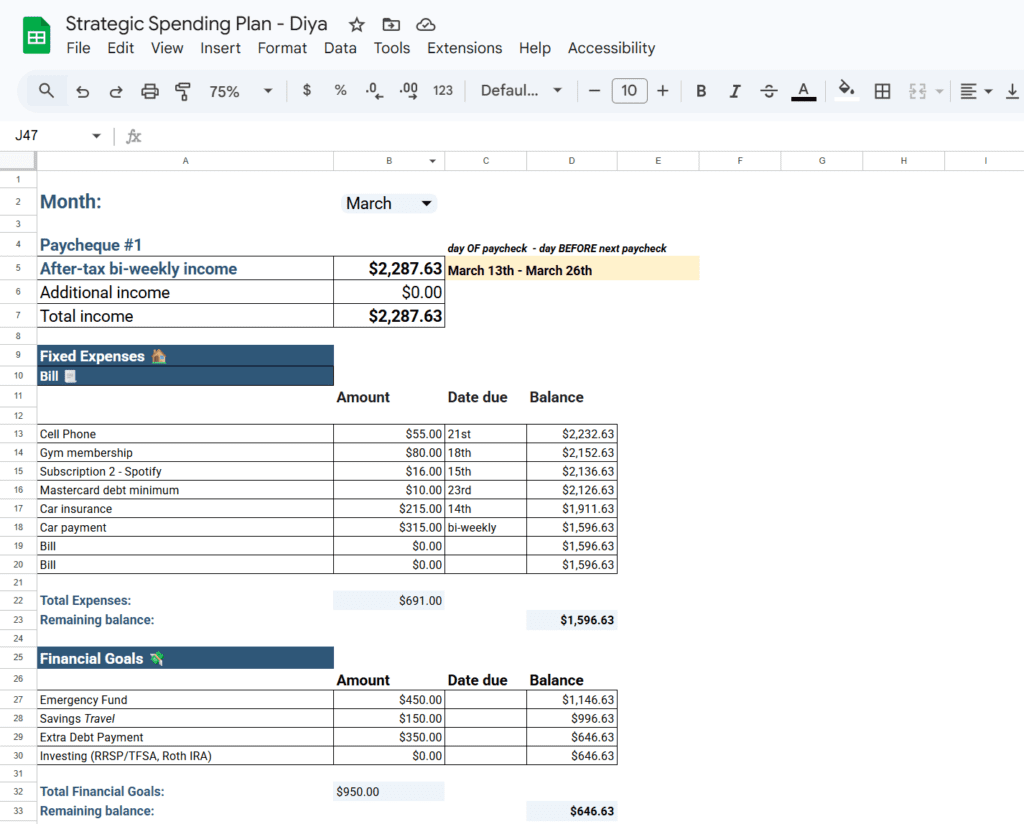

We created a paycheck-by-paycheck budgeting system, which is one of the most effective ways to budget your money (and my personal favorite).

Instead of guessing where her money should go, she now had:

- a clear plan for every paycheque

- exact allocations for bills, savings, and debt

- visibility into how much she could spend without guilt

Diya had tried so many budgeting templates before, but they never stuck.

This time was different because the plan actually reflected her real life and how her money flowed.

I’ll be going deeper into why the paycheck-by-paycheck budgeting structure works so well in a future post.

If you want to follow this exact structure, you can use my budgeting template here.

We also:

✔️ Created a debt repayment tracker

✔️ Built a $5,000 emergency fund plan

✔️ Added savings buckets for travel and self-care

Because sustainable budgeting isn’t about restriction. It is about building a system you can actually follow.

Most importantly, we worked on her relationship with money, not just her numbers.

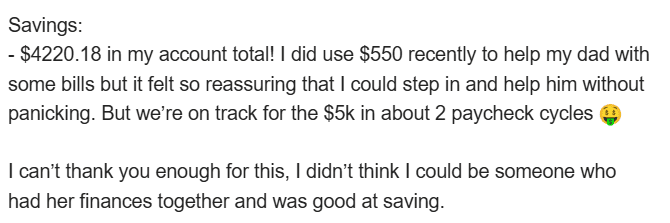

Budgeting Results After 6 Months

At Diya’s 6-month check-in, here’s what changed:

- Nearly paid off her $3,900 credit card

- Saved $4,200 (from $0)

- Built consistent financial habits

She is now on track to:

- be completely debt-free

- have $16,000 in savings by the end of 2026!

What This Budgeting Example Shows

If you’re trying to learn how to budget your money, here’s the key takeaway:

Diya didn’t have an income problem.

She had:

- no system for her money

- emotional patterns driving her spending

- cultural experiences shaping her financial behaviour

Once we addressed those, everything changed.

How to Budget Money in Canada (Final Thoughts)

If you’re asking:

👉 “Why can’t I stick to a budget?”

👉 “Where is my money going?”

It’s likely not a discipline issue.

It’s that:

- your budget isn’t realistic

- your spending isn’t being examined

- your emotional patterns aren’t being addressed

A good budgeting plan should:

- reflect your real life

- include flexibility

- support your goals and your enjoyment

If you want help creating a personalized budgeting plan, paying off debt, and building savings in a way that actually works for your life:

👉 You can apply for 1:1 money coaching here.